5 Reasons to Refinance Your Home in 2026

When most people hear the word refinance, one idea comes to mind: lower my interest rate, lower my payment. Done.

And while that's absolutely the most common reason homeowners refinance — and a very good one — it's far from the only one.

The better way to think about refinancing is as a financial tool. Depending on what's happening in your life, your budget, and your long-term goals, the right refinance can unlock flexibility, reduce risk, eliminate unnecessary costs, or restructure your loan to better fit who you are today compared to when you first signed.

Below are five of the most common and impactful reasons homeowners refinance in 2026 — including a few that may surprise you — along with honest guidance on which type of refinance applies to each situation.

1. Lower Your Interest Rate and Monthly Payment

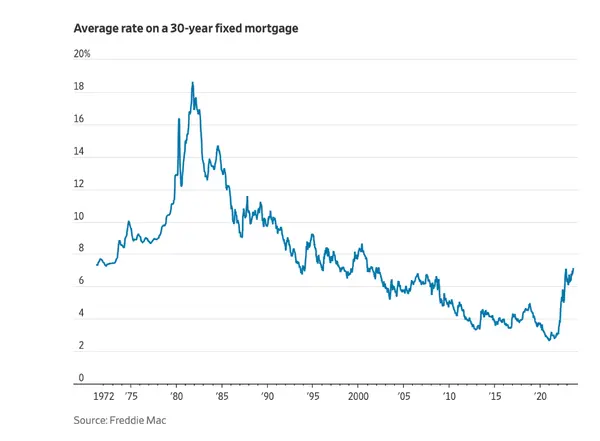

This is where most refinance conversations start, and for good reason. If current mortgage rates are meaningfully lower than the rate on your existing loan, refinancing can directly reduce your monthly payment and free up real cash flow every single month for years to come.

The product used here is typically a rate-and-term refinance — a new loan that replaces your current mortgage with a different interest rate, a different loan term, or both. The goal is a better structure, a lower payment, or both at once.

This tends to make sense when:

- Current rates are at least 0.5%–1% lower than your existing rate

- Your credit profile is stronger now than when you originally financed, which could unlock a better rate regardless of market movement

- You're currently in an adjustable-rate mortgage (ARM) and want the certainty of a fixed rate before your adjustment period hits

- You want to lower your monthly payment without touching your equity

For veterans with existing VA loans, the VA IRRRL (Interest Rate Reduction Refinance Loan) is an even more streamlined version of this — no appraisal required in most cases, no income re-verification, and one of the lowest funding fees in the mortgage industry. If you have a VA loan from 2022–2024 at a rate above 6.5%, the math on an IRRRL is worth running right now.

2. Access Your Home Equity for Big Goals

Home equity isn't just a number that shows up on your net worth statement. It's a real, usable financial resource — and for many North Texas homeowners who've benefited from significant appreciation over the last several years, it may be larger than you think.

A cash-out refinance allows you to replace your current mortgage with a new, larger loan and receive the difference in cash. That money can be used for essentially any purpose, though the most common uses are:

- Home renovations — kitchens, primary bathrooms, additions, and outdoor living spaces that improve both quality of life and resale value

- Major life expenses — tuition, medical costs, or other significant one-time obligations

- Debt consolidation — paying off higher-interest balances with lower-cost mortgage dollars

- Investment — funding down payments on investment properties, business capital, or other long-term wealth-building strategies

Quick Example:

Your home appraises at $480,000. Your current mortgage balance is $310,000. You have $170,000 in equity. A cash-out refinance could allow you to access a meaningful portion of that equity — depending on loan type and guidelines, typically up to 80%–90% of your home's appraised value — while the rest stays invested in the property.

If you want to access equity but aren't ready to replace your entire mortgage, a HELOC (Home Equity Line of Credit) is worth considering as an alternative. A HELOC sits alongside your existing mortgage as a separate revolving line of credit — more like a financial safety net or on-demand resource — rather than a full loan replacement.

Clarity Home Lending can walk you through both options side by side so you can see exactly which structure serves your goals.

3. Consolidate High-Interest Debt Into One Payment

This is one of the most financially impactful refinance strategies, and one of the most underused.

Consider the math: credit card interest rates are currently averaging well above 20% APR. Personal loan rates aren't far behind. If you're carrying significant balances at those rates while simultaneously sitting on home equity financed at a 6% or 7% mortgage rate, the math strongly favors restructuring.

A cash-out refinance used for debt consolidation can:

- Dramatically reduce the interest rate on what you owe, replacing 20%+ credit card rates with your mortgage rate

- Simplify your monthly finances by consolidating multiple minimum payments into a single monthly mortgage payment

- Improve monthly cash flow by replacing high minimum payments with a lower blended payment

- Provide a defined payoff timeline — unlike revolving credit card debt, a mortgage has a fixed term

One thing to be clear about: debt consolidation through a refinance is not free money — it's a strategic restructuring of your existing obligations. The goal is to reduce total interest cost over time and create a more manageable monthly financial picture. It works best when paired with a commitment not to re-accumulate the high-interest debt that was paid off.

Clarity Home Lending will model this scenario concretely for you — showing the before and after of your monthly payments, the total interest comparison, and the break-even timeline — so you can make an informed decision rather than a guess.

4. Remove PMI Once You've Built Enough Equity

Private Mortgage Insurance (PMI) is a monthly charge that applies to conventional loans originated with less than 20% down. It exists to protect the lender — not you — and it adds anywhere from 0.5% to 1.5% of your original loan amount to your annual housing costs, paid monthly, until you reach sufficient equity.

What many homeowners don't realize is that PMI doesn't have to stay. If your home's value has increased and/or you've paid down your balance meaningfully since you bought, you may already have enough equity to eliminate it.

Here's what that looks like in practice:

You purchased your home at $320,000 with 5% down ($16,000), leaving a $304,000 loan and a PMI obligation. Three years later, your home has appreciated to $375,000 and your loan balance has dropped to $285,000. You now have approximately $90,000 in equity — well above the 20% threshold on your home's current value. PMI doesn't need to be part of your payment anymore.

In some cases, you can request PMI removal directly from your servicer once you reach 20% equity based on your original purchase price. But if your home has appreciated, a refinance is often the cleaner and faster path — because it uses the current appraised value, not the original purchase price, to establish your equity position. And if refinancing also produces a lower rate, you get two improvements for the cost of one transaction.

The monthly savings from removing PMI alone can run $150–$400 per month depending on your loan size — that's $1,800–$4,800 back in your budget annually, every year, with no change to your lifestyle.

5. Change Your Loan Term to Match Where You Are in Life

Not every refinance is about paying less money each month. Sometimes the right move is about aligning your mortgage with what actually matters to you right now.

A rate-and-term refinance gives you the ability to reshape your loan's structure without necessarily accessing equity or changing your rate dramatically. The two most common term adjustments are:

Shortening Your Term

Moving from a 30-year mortgage to a 15-year mortgage means a higher monthly payment, but it also means:

- Significantly less total interest paid over the life of the loan — often hundreds of thousands of dollars less

- Building equity at a dramatically faster rate

- Owning your home free and clear years sooner — a powerful goal for homeowners approaching retirement or wanting to eliminate the payment before a child starts college

Extending Your Term

If your financial picture has changed and monthly cash flow is the priority right now, resetting to a new 30-year term can reduce your monthly obligation and create breathing room in your budget. This isn't the right move for everyone, but there are real situations — career transition, a growing family, a business investment — where the flexibility of a lower mandatory payment is genuinely valuable.

There's no universal right answer here. The best term structure for you depends on your income, your goals, your timeline, and what you want your financial life to look like in 5, 10, and 20 years. That's exactly the kind of conversation Clarity Home Lending's loan officers are built for — not a one-size-fits-all recommendation, but a real analysis of your specific situation.

Refinance Options at a Glance

Depending on your current loan type and your goals, your refinance will likely fall into one of these categories:

| Refinance Type | Best For |

|---|---|

| Rate-and-Term Refinance | Lowering rate, adjusting term, removing PMI, moving from ARM to fixed |

| Cash-Out Refinance | Accessing equity, consolidating debt, funding major expenses |

| VA IRRRL | Veterans with existing VA loans seeking a lower rate/payment — streamlined process |

| FHA Streamline Refinance | FHA loan holders seeking a lower rate with minimal documentation |

Not every option fits every homeowner. But most homeowners have at least one refinance path that's worth running the numbers on — and in many cases, the math is more compelling than people expect.

Frequently Asked Questions

How much equity do I need to refinance?

It depends on the loan type. Conventional cash-out refinances typically require at least 20% equity remaining after the transaction. Rate-and-term refinances can work with less. VA IRRRL and FHA Streamline refinances have their own distinct guidelines. Clarity Home Lending can assess your specific equity position and identify which paths are available to you.

What does a refinance cost?

Closing costs on a refinance typically run 2%–5% of the loan amount. In many cases, these costs can be rolled into the new loan — meaning no out-of-pocket expense at closing. The VA IRRRL in particular can often be structured with zero cash due at closing.

Does refinancing only make sense when rates drop?

Not at all. Rate reduction is one of five reasons covered here — and others, like removing PMI, consolidating debt, or adjusting your loan term, may make sense regardless of where rates are relative to your current loan.

How do I know if it's "worth it"?

The clearest framework: what problem does the refinance solve, and what does it cost to solve it? Clarity Home Lending will show you the monthly difference, the total cost of the refinance, and the break-even point — so you can make a real decision, not a guess.

Will refinancing restart my loan at 30 years?

Only if you choose a 30-year term on the new loan. You have flexibility on term length, and Clarity Home Lending will show you how different term choices affect both your monthly payment and your total cost over time.

What credit score do I need?

Most conventional refinances require a minimum score of 620, with higher scores unlocking better rates. VA and FHA refinance options often have more flexibility. Your specific score and profile will shape which products are available to you and at what rate.

How long does a refinance take?

Timeline varies by loan type, property, and documentation complexity. A VA IRRRL typically closes in 14–21 days. Conventional and cash-out refinances often run 21–35 days. Clarity Home Lending moves efficiently and keeps you updated throughout.

Ready to See What Makes Sense for You?

The best refinance decision starts with a real conversation — not a generic rate quote from a website, but a genuine review of your loan, your goals, and the options that actually apply to your situation.

Clarity Home Lending offers free, no-obligation refinance consultations. In about 15 minutes, a loan officer can review your current loan, tell you which refinance paths are available to you, and model the numbers clearly so you can decide from a position of information rather than uncertainty.

Recent Posts

President | Senior Loan Officer | License ID: NMLS 621901

+1(972) 210-9264 | greg@clarityhomelending.com