Where Mortgage Rates Stand in June 2026 — and What's Driving Them

If you've been watching mortgage rates this year hoping for a return to the 3% loans of 2020 and 2021, June 2026 has been a reminder that the market doesn't always move the way we expect. After a promising start to the year, rates reversed course this spring — and they're now sitting noticeably higher than where many forecasters thought we'd be by mid-summer.

Here's an honest, in-depth look at where rates are right now, how we got here, what's pushing them around, and what it all means if you're thinking about buying or refinancing a home in North Texas.

Where Rates Stand Right Now

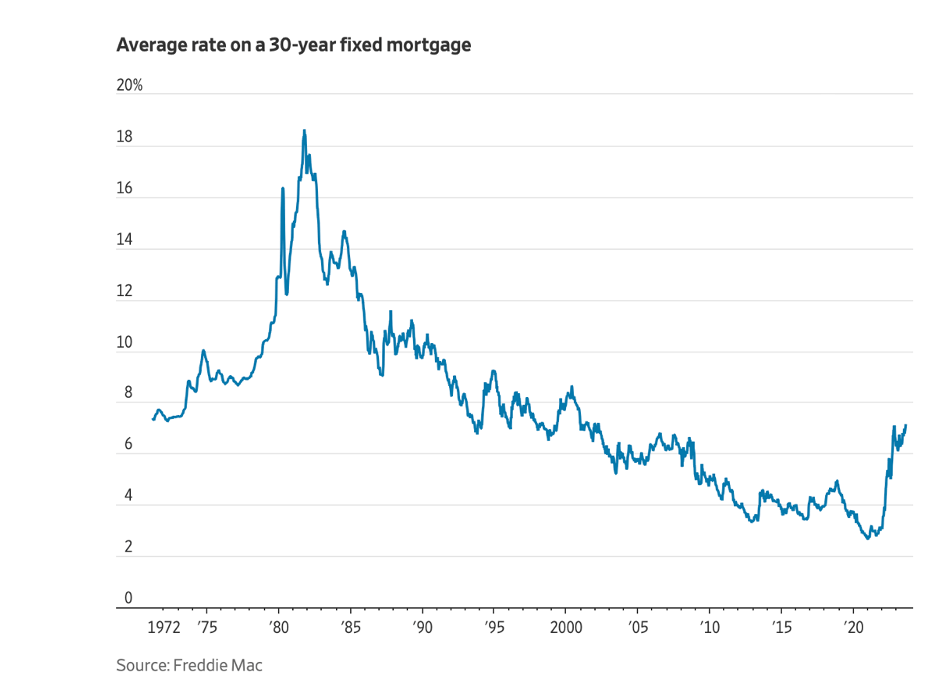

As of late June 2026, the 30-year fixed-rate mortgage is hovering right around the mid-6% range. Freddie Mac's closely watched weekly survey puts the national average 30-year fixed at roughly 6.49%, essentially flat over the past six weeks, while the 15-year fixed sits near 5.84%.

Different surveys show slightly different numbers — daily trackers from Bankrate, Zillow, and the Mortgage Bankers Association have the 30-year landing anywhere from the low-6% to mid-6% range depending on the day and methodology — but the takeaway is consistent: rates have settled into a fairly stable groove in the mid-6s after a volatile spring.

A few quick reference points for late June 2026:

- 30-year fixed: ~6.5%

- 15-year fixed: ~5.7%–5.85%

- 5/1 ARM: ~6.4%

- 30-year refinance: typically a touch higher than purchase, around 6.7%

For perspective, a year ago the 30-year fixed averaged about 6.77% — so despite this spring's jump, we're still slightly below where we were in mid-2025.

How We Got Here: The 2026 Story

The path to today's rates is the part most headlines skip, and it's worth understanding.

Coming into 2026, the mood was optimistic. Mortgage rates had fallen by roughly a full percentage point between January 2025 and January 2026, and as recently as mid-April, the 30-year fixed had dipped below 6% — the lowest level since September 2022. Many forecasters expected the Federal Reserve to begin cutting rates as the year went on, with mortgage rates drifting lower alongside.

Then the picture changed. A conflict in the Middle East — the war involving Iran — sent oil prices surging, which fed directly into inflation fears. From mid-April onward, rates climbed by more than half a percentage point as investors abandoned their expectations of Fed rate cuts. The energy shock, combined with inflation data that refused to cooperate, pushed mortgage rates from the high-5% range back up into the mid-6s, where they've stabilized.

In short: 2026 didn't deliver the steady decline many had penciled in. Instead, global events rewrote the script in a matter of weeks.

What's Actually Driving Rates

It's a common misconception that the Federal Reserve sets mortgage rates directly. It doesn't. Mortgage rates track much more closely with the bond market — specifically the 10-year Treasury yield, which has been hovering around 4.5%–4.6%. When investors get nervous about inflation, they demand higher yields on bonds, and mortgage rates follow.

Three forces are doing most of the work right now:

1. Stubborn inflation. May's Consumer Price Index showed inflation running at about 4.2% annually — the highest pace in more than three years, and well above the Fed's 2% target. As long as inflation stays hot, there's little room for rates to fall meaningfully.

2. A resilient economy. The May jobs report (released in early June) showed employment growing by about 172,000 jobs, beating expectations. A strong labor market is good news for the economy, but it gives the Fed less reason to ease — which keeps upward pressure on rates.

3. The Fed's posture. At its June meeting, the Federal Reserve held its benchmark rate steady, as widely expected. But the surprise came in its tone: the updated projections showed that a majority of policymakers now expect a rate hike later this year — not a cut. That hawkish shift caught markets off guard and nudged rates upward, even though the Fed didn't move at the meeting itself.

What It Means for North Texas Buyers and Homeowners

Numbers on a national chart are one thing — what they mean for your situation is another. Here's how to think about it if you're in the DFW market:

If you're buying: Yes, rates are higher than the historic lows of a few years ago. But it's worth remembering that those sub-3% rates were an extraordinary outlier, produced by emergency Fed measures during the pandemic — not a normal baseline to wait for. Most experts expect rates to stay above 6% for the foreseeable future, so building your plans around a return to 3% isn't a realistic strategy. The better approach is to focus on what you can control: your credit, your down payment, and finding the right loan structure for your goals.

North Texas also has a structural advantage worth noting: it remains one of the fastest-growing regions in the country, with strong job growth and a steady stream of new residents. That demand keeps the local housing market active, which is part of why timing the market perfectly matters less than getting into a home you can comfortably afford.

If you're refinancing: The old rule of thumb is that a refinance becomes worth considering when you can shave roughly half a percentage point to a full point off your current rate. If you bought when rates were near their 2023 or 2025 peaks, it may be worth running the numbers. Just remember to factor in closing costs and how long you plan to stay in the home — you need to remain long enough to recoup those upfront costs for the refinance to pay off.

If you're tapping equity: With home values across DFW having climbed substantially in recent years, many homeowners are sitting on significant equity. A home equity line of credit (HELOC) can be a flexible way to access that value for renovations, debt consolidation, or major expenses — without disturbing the low rate on your first mortgage, if you have one.

Practical Moves in a Mid-6% Market

You can't control the bond market or the Fed, but you have more influence over your own rate than you might think:

- Strengthen your profile. A higher credit score and a larger down payment can meaningfully lower the rate a lender can offer you. Small improvements here often matter more than waiting for the market to shift.

- Shop around. Rates and fees vary from lender to lender. Getting personalized quotes from several lenders is one of the simplest ways to save real money — potentially thousands over the life of the loan.

- Consider the loan structure. A 15-year fixed carries a lower rate and saves enormous interest over time, if you can handle the higher monthly payment. An adjustable-rate mortgage may make sense if you expect to move or refinance before the fixed period ends. The right choice depends entirely on your timeline and budget.

- Ask about points. If you have extra cash on hand, paying discount points upfront can buy down your rate for the life of the loan. Whether that math works depends on how long you'll keep the mortgage.

The Outlook for the Rest of 2026

The consensus among housing economists is that rates are likely to stay relatively elevated — above 6% — through the rest of 2026 and possibly into the next few years. With inflation sticky and the labor market resilient, the conditions for a meaningful drop simply aren't in place yet.

That said, the situation is fluid. If the Middle East conflict resolves and energy prices ease, and if inflation data begins to cool, the pressure on rates could let up. As one chief economist put it, mortgage rates are unlikely to fall meaningfully until inflation cools and long-term Treasury yields move decisively lower. For now, the smart money is on stability in the mid-6% range rather than a sharp move in either direction.

The bottom line: waiting on the sidelines for a dramatic rate drop carries its own risks, especially in a growing market like North Texas where home prices and demand stay strong. The best decision is rarely about timing the market perfectly — it's about understanding your own numbers and working with a lender who can help you find the right loan for where you are today.

If you'd like a personalized look at what you'd qualify for in today's market, we're always glad to walk through the numbers with you — no pressure, just clarity.

Recent Posts

President | Senior Loan Officer | License ID: NMLS 621901

+1(972) 210-9264 | greg@clarityhomelending.com