North Texas Market & Interest Rate Update — July 2026

Where Rates Stand Right Now

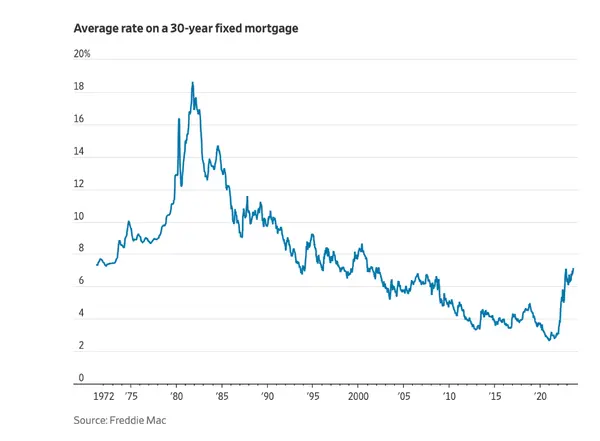

Mortgage rates have been stuck in a frustratingly tight band for most of the summer — and last week added some volatility. Here's what the data shows:

As of July 9, 2026, the 30-year fixed-rate mortgage averaged 6.49% according to Freddie Mac's weekly survey — up from 6.43% the prior week. The 15-year fixed-rate mortgage averaged 5.82%, also slightly higher week-over-week.

On an intraday basis, purchase mortgage rates have ranged from the mid-6.6s to the high-6.7s this week, with July 9 showing an average of 6.716% for a 30-year fixed purchase loan and 6.785% for a 30-year refinance, per Zillow data.

What pushed rates higher this week? Mortgage rates were driven upward by renewed U.S.-Iran conflict, as both sides exchanged strikes over the July 4th holiday weekend. Rising oil prices tied to the Middle East situation are putting upward inflationary pressure throughout the economy — and mortgage rates track 10-year Treasury yields, which are highly sensitive to inflation signals.

What's the Fed doing? Rates drifted higher after the June Federal Reserve meeting — not because the Fed held rates steady (that was widely expected), but because of the hawkish tone in the updated economic projections. The majority of Fed policymakers now expect a rate hike will be necessary later this year, not a cut, as inflation remains well above the 2% target.

What does this mean for the rest of July? With a Fed rate cut off the table, mortgage rates are likely to remain near current levels through the end of the month. Any drops tied to specific news events are expected to be short-lived. Most experts expect rates to hover between 6% and 7% for the foreseeable future, with a brief dip below 6% possible but unlikely to hold.

The DFW Housing Market in July 2026

Prices: The Dallas-Fort Worth-Arlington metro posted a median list price of $435,999 in May 2026, down about 0.9% year-over-year. Median seller price cuts have averaged $12,500 (about 3% off initial listing price) in DFW, reflecting buyers' increased negotiating leverage.

Inventory and Days on Market: DFW's median days on market hit 51 days in June 2026 — meaningfully longer than the frenetic pace of 2021–2022 and a clear signal that buyers have time to shop carefully. About 26% of Dallas-area listings had at least one price reduction in May 2026, slightly above the national average.

Buyer vs. Seller Market: The DFW market is more balanced than it was a few years ago, with some sources reporting buyer's market conditions. Redfin reported roughly twice as many sellers as buyers in early summer 2026.

Fort Worth Showing Early Recovery: While Dallas prices are still seeing year-over-year declines of around 1.3%, Fort Worth-Arlington is beginning to show early signs of recovery, with year-over-year declines narrowing to just 0.4%.

The Long-Term Case for DFW: DFW's average home price near $420,000 remains roughly 30% cheaper than Austin and about half the cost of major California metros. Mortgage payments consume about 15% of median household income in DFW, compared to more than 25% nationally — a gap that continues to drive in-migration. More than 100,000 relocators arrive annually from higher-cost markets, and projections show more than 25,000 new DFW households forming in 2026 alone.

What This Means for Buyers and Sellers Right Now

For buyers: This is one of the better negotiating environments DFW has seen in years. More inventory, longer days on market, motivated sellers, and builder incentives (including rate buydowns) mean qualified buyers have real leverage. The rate environment isn't ideal, but the pricing correction partially offsets it — and waiting for rates to drop while prices recover is a risk worth calculating.

For sellers: Realistic pricing from day one is non-negotiable right now. Homes that come in correctly priced are still moving. Homes that list high and chase the market down are sitting and losing momentum. Your agent's market knowledge at the micro-neighborhood level has never mattered more.

For homeowners: If you locked in a rate above 7% in 2022–2023, the IRRRL or refinance math at today's 6.4%–6.5% range may not be as dramatic as it would have been if rates had dropped further. Keep monitoring. The moment rates make a meaningful move lower, the window to act will be competitive.

Recent Posts

President | Senior Loan Officer | License ID: NMLS 621901

+1(972) 210-9264 | greg@clarityhomelending.com