What Credit Score Do You Need to Buy a House?

What Credit Score Do You Need to Buy a House?

Your credit score is one of the first things a mortgage lender will review when you apply to buy a home. However, there is no single credit score required for every borrower or every mortgage program.

Some buyers may qualify with a credit score in the 500s, while others may need a higher score depending on the loan type, down payment, debt-to-income ratio and overall financial profile.

A higher credit score can generally help you qualify for better loan terms, but a less-than-perfect score does not necessarily mean homeownership is out of reach.

Why Does Your Credit Score Matter?

A credit score is designed to estimate how likely you are to repay borrowed money. Mortgage lenders use your credit score and credit history to help evaluate the risk associated with approving your loan.

Your credit can affect:

-

Whether you qualify for a mortgage

-

Which loan programs are available

-

Your mortgage interest rate

-

Your required down payment

-

Your private mortgage insurance cost

-

Whether additional documentation or reserves are required

Your credit score is important, but it is only one part of the mortgage application.

Lenders will also review your:

-

Income and employment history

-

Monthly debt obligations

-

Available funds for closing

-

Down payment

-

Cash reserves

-

Recent payment history

-

Bankruptcies, foreclosures or other major credit events

-

Property type and intended occupancy

A borrower with a lower credit score may still qualify when the rest of the application is strong.

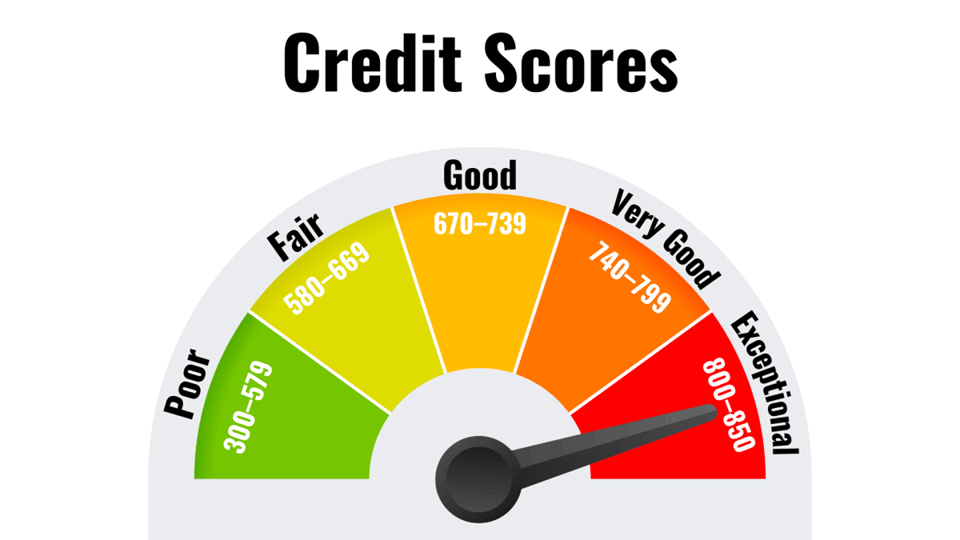

Minimum Credit Score for a Conventional Loan

Conventional loans are mortgages that are not insured by a government agency.

For many years, buyers were commonly told that they needed at least a 620 credit score to qualify for a conventional mortgage. However, current automated underwriting guidelines are more nuanced.

Fannie Mae’s Desktop Underwriter and Freddie Mac’s Loan Product Advisor may evaluate a borrower’s complete credit profile without applying a universal minimum score to every loan receiving an acceptable automated underwriting recommendation.

That does not mean every buyer with a score below 620 will qualify.

The automated underwriting system may consider several factors, including:

-

Payment history

-

Outstanding debt

-

Credit utilization

-

Down payment

-

Debt-to-income ratio

-

Cash reserves

-

Recent credit inquiries

-

Serious delinquencies or other derogatory credit

Individual lenders may also establish their own minimum credit-score requirements, which are commonly called lender overlays.

A lower score may therefore be eligible under an agency’s general guidelines but still fall below a particular lender’s internal requirements.

Minimum Credit Score for an FHA Loan

FHA loans are insured by the Federal Housing Administration and are often considered by buyers with limited savings or lower credit scores.

Under FHA’s baseline requirements:

-

A credit score of 580 or higher may qualify for the minimum 3.5% down payment.

-

A credit score between 500 and 579 generally requires at least 10% down.

-

A score below 500 is generally not eligible for standard FHA-insured financing.

These are FHA’s minimum program standards. Mortgage lenders may require higher scores based on their own underwriting policies.

Your recent payment history also matters. Having a qualifying numerical score does not automatically overcome recent late payments, unpaid obligations or other significant credit concerns.

Minimum Credit Score for a VA Loan

VA loans are available to eligible veterans, active-duty service members and certain surviving spouses.

The Department of Veterans Affairs does not establish a universal minimum credit score for its home loan guaranty program. Instead, lenders evaluate the borrower’s overall creditworthiness and ability to repay the loan.

However, individual VA lenders may establish their own minimum score requirements.

A lender may also review:

-

Recent housing payment history

-

Collections and charged-off accounts

-

Bankruptcy or foreclosure history

-

Debt-to-income ratio

-

Residual income

-

Employment stability

-

Available funds after closing

A lower credit score does not automatically disqualify an eligible veteran, but the complete loan file must still meet the lender’s and VA’s underwriting requirements.

Minimum Credit Score for a USDA Loan

USDA loans can provide 100% financing for eligible borrowers purchasing qualifying properties in designated areas.

A validated score of 640 or higher is generally considered an acceptable credit benchmark for USDA guaranteed financing. However, USDA underwriting does not necessarily make 640 an absolute cutoff for every borrower.

Applicants with lower scores may still be considered, but the loan may require additional credit analysis, manual underwriting or stronger supporting factors.

USDA lenders can also impose requirements that are more restrictive than the agency’s baseline guidelines.

In addition to credit, USDA eligibility depends on factors such as:

-

Household income limits

-

Property location

-

Primary-residence occupancy

-

Repayment ability

-

Federal debt status

-

Overall credit history

Minimum Credit Score for a Jumbo Loan

A jumbo loan is a mortgage that exceeds the conforming loan limit applicable to the property.

There is no single credit-score requirement for all jumbo loans. Because these mortgages are not generally sold under standard conforming guidelines, requirements can vary significantly among lenders and investors.

Jumbo borrowers are often expected to have:

-

Strong credit

-

A larger down payment

-

Lower debt-to-income ratios

-

Substantial cash reserves

-

Stable and well-documented income

Some jumbo programs may accept scores in the upper 600s, while others may require a score of 700, 720 or higher. The required score can also depend on the loan amount, property type and down payment.

What Is Considered a Good Credit Score for Buying a House?

Qualifying for a mortgage and receiving the best available pricing are not always the same thing.

You may be approved with a lower credit score, but a higher score can potentially provide:

-

A lower interest rate

-

Lower private mortgage insurance

-

More loan-program options

-

A smaller required down payment

-

Greater flexibility with debt-to-income ratios

-

A stronger automated underwriting result

There is no universal score that guarantees the best mortgage rate. Pricing also depends on the loan program, down payment, loan amount, property type, occupancy and current market conditions.

The best approach is to have a lender compare multiple loan options using your actual financial information.

Is the Credit Score on Your Banking App Accurate?

The score shown by a bank, credit card company or credit-monitoring application may not be the same score used for your mortgage application.

Consumers can have several credit scores because different companies use different scoring models and versions. The score can also vary based on which credit bureau supplied the underlying information.

A mortgage lender generally obtains a residential mortgage credit report containing information from Equifax, Experian and TransUnion.

It is therefore normal for your mortgage credit score to differ from the score shown by a consumer application.

Can You Buy a House Without a Traditional Credit Score?

Having little or no traditional credit does not always prevent you from buying a home.

Certain mortgage programs may permit alternative or nontraditional credit documentation. This can include a documented history of payments such as:

-

Rent

-

Utilities

-

Insurance

-

Cellphone service

-

Other recurring obligations

The availability of nontraditional credit underwriting depends on the loan program, lender and borrower’s complete financial profile.

How Can You Improve Your Credit Before Buying a House?

Improving your score does not always require years of work. Depending on your credit profile, targeted changes may help strengthen your mortgage application.

Consider the following steps:

Pay every account on time

Payment history is one of the most influential components of a credit score. Avoid new late payments before and during the mortgage process.

Reduce credit card balances

High balances in relation to your credit limits can lower your score. Paying down revolving debt may improve your credit utilization and reduce your monthly obligations.

Review your credit reports

Check your reports for inaccurate balances, duplicate accounts, unfamiliar activity or incorrect late payments. Dispute legitimate errors directly with the applicable credit bureau.

Avoid opening unnecessary accounts

New credit inquiries and recently opened accounts may affect your score. Avoid financing vehicles, furniture or other large purchases while preparing to buy a home.

Do not close accounts without guidance

Closing a credit card can reduce your available credit and increase your utilization percentage. Speak with your loan officer before making major changes to established accounts.

Keep old accounts in good standing

Longer credit histories can be beneficial. Maintaining older accounts responsibly may help support your overall credit profile.

Speak with a lender before paying collections

Paying a collection does not always produce an immediate score increase, and different loan programs treat collection accounts differently. Ask your loan officer to review the account before moving money or negotiating a settlement.

Can a Co-Borrower Help if Your Credit Score Is Low?

Adding a co-borrower may help when additional qualifying income is needed, but it does not automatically solve a credit-score issue.

The lender must review the credit, income, debts and financial obligations of everyone applying for the loan. Depending on the program, a lower score belonging to one borrower may still affect eligibility, pricing or mortgage insurance.

A co-borrower should be added because the arrangement makes financial and legal sense—not simply as a quick credit workaround.

Should You Wait Until Your Credit Is Perfect?

You do not necessarily need perfect credit to become a homeowner.

Waiting may be beneficial when improving your score could meaningfully reduce your interest rate, mortgage insurance or required down payment. In other situations, a buyer may already qualify for an affordable mortgage and decide that purchasing now better supports their goals.

The decision should be based on actual loan options rather than assumptions about what score is required.

Find Out Where You Stand

Online credit information can provide a general starting point, but it cannot determine whether you qualify for a specific mortgage.

Clarity Home Lending can review your credit, income, debts, down payment and homebuying goals to help identify the loan programs that may be available to you.

Even if your credit is not where you want it to be, reviewing it early can give you a clear plan for moving forward.

Contact Clarity Home Lending to begin your mortgage preapproval and learn what options may be available based on your complete financial profile.

This information is provided for educational purposes only and is not a commitment to lend. Credit-score requirements, interest rates, mortgage insurance costs and underwriting standards vary by loan program, lender, investor and individual borrower circumstances. All loans are subject to credit review and underwriting approval.

Recent Posts

President | Senior Loan Officer | License ID: NMLS 621901

+1(972) 210-9264 | greg@clarityhomelending.com